Are tariffs working?

#177 - Trade deficits, decoupling, and the limits of tariff policy

Hello friends, I hope you had a great week!

I’ll be honest: I had a different post ready for today.

I’ve been sitting on this tariff piece for a few weeks, wondering whether to publish it at all. The topic felt like it had crested: debated to exhaustion, turned into a political Rorschach test where everyone sees exactly what they came in expecting to see. I figured I’d move on.

Then, last Thursday, the Supreme Court handed down a 6-3 ruling striking down a significant chunk of Trump’s tariffs. Chief Justice Roberts, writing for the majority, held that the emergency powers law Trump used (i.e. the “International Emergency Economic Powers Act”) does not authorize the president to unilaterally impose tariffs of unlimited amount, scope, and duration without clear congressional authorization. Trump called the decision “a disgrace.” Within hours, he signed a new executive order imposing a 10% global tariff under a different law (Section 122 of the Trade Act of 1974) now being raised to 15%. That one expires in 150 days, which means Congress will have to vote on whether to extend it right before the 2026 midterms. The legal reshuffling happened faster than most analysts expected.

So here we are. The topic has a way of doing this.

A quick caveat before we go further: this is one of the fastest-moving policy stories in recent memory. By the time you read this, something may have shifted again: refund litigation is unfolding in lower courts, new tariff orders are being drafted, and trading partners are recalibrating their responses in real time. I’ll do my best to flag what’s settled analysis versus what’s still in motion.

What I find interesting is that the ruling doesn’t actually resolve the underlying questions but it just reshuffles the legal deck. The scoreboards don’t change. The structural arguments don’t change. Whether tariffs reduce deficits, rebuild manufacturing, or create strategic resilience remains exactly as contested today as it was the day before the ruling.

My view is that tariffs are a very specific tool. They can change prices at the border fast. They can push companies to re-source, re-route, and re-negotiate. They can also trigger retaliation and raise input costs for domestic producers. They do not reliably change the underlying forces that drive a country’s total trade balance. They do not magically recreate a manufacturing base when labor, capital, regulation, and supply chains are pointing elsewhere. In practice, they’re better at nudging decisions at the margin than “fixing” big structural problems.

So the right question is: which outcomes did we actually get, with the latest data in hand?

I’ll treat tariffs like an instrument, not a moral stance, and look at three scoreboards: trade deficits, manufacturing and jobs, and strategic decoupling. Then I’ll zoom out to what the EU and India are doing, because the U.S. case is loud but not unique.

What Does “Working” Even Mean?

Before looking at numbers, I want to clean up the definition.

When someone says “tariffs are working,” I always ask: working for what?

There are at least three distinct objectives that get mixed together. The first is the macro objective: reduce the overall trade deficit, the headline number politicians point to. The second is the industrial objective: rebuild domestic manufacturing capacity and jobs, meaning more factories, more output, more durable employment growth in tradable sectors. The third is the strategic objective: reduce dependence on geopolitical rivals, especially China, meaning lower import shares from a specific country, more diversified supply chains, and less vulnerability to coercion.

These objectives overlap, but they are not the same. In fact, they can move in opposite directions.

You can reduce a bilateral deficit with one country while the overall deficit stays high. You can increase factory construction while manufacturing employment falls because automation dominates. You can decouple from one rival while increasing dependence on a different region. This is why tariff debates often feel circular, and one of those arguments where “Everyone is right”.

One side points to a falling China import share and says: success. The other points to a still-large overall deficit and flat manufacturing jobs and says: failure. Both can be right, depending on the metric. Most arguments are really just people talking past each other with different scoreboards in mind.

My starting position is pragmatic. A tariff is a price intervention at the border. Change relative prices, and you change sourcing decisions: that part is mechanical. What tariffs do not directly touch are a country’s savings rate, fiscal deficits, labor costs, productivity growth, or technology leadership. So if someone expects tariffs to do the work of macro policy or industrial policy, disappointment is baked in.

With that frame in place, let’s look at each scoreboard in turn.

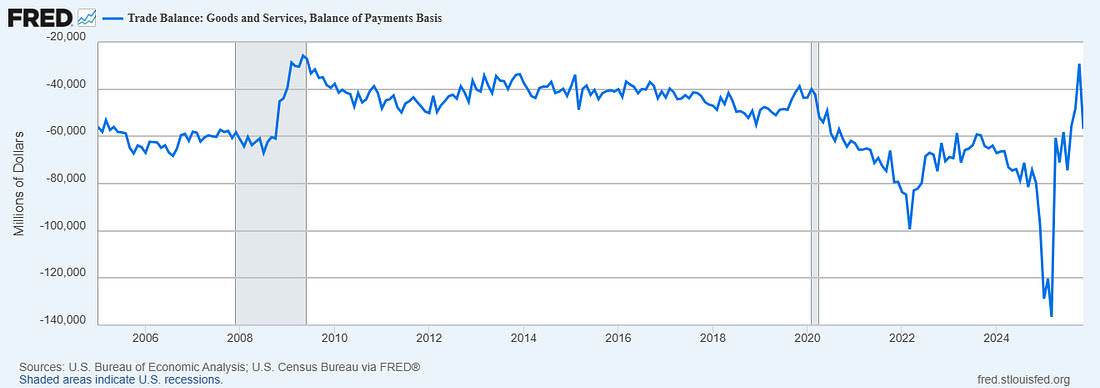

Trade Deficits: Bilateral Win, Macro Stalemate

If the goal was to reduce the overall U.S. trade deficit, the data is unambiguous: tariffs did not deliver that outcome.

The U.S. goods trade deficit reached record levels in 2022 and remains structurally high in fact, Bureau of Economic Analysis data released just before the Supreme Court ruling showed the gap between U.S. goods imports and exports actually increased by 5.7% in 2025, despite the full weight of IEEPA tariffs being in effect all year. It has fluctuated with growth cycles, but it has not collapsed under tariff pressure, and this is not surprising once you understand the mechanism. A country’s total trade deficit is the mirror image of its savings-investment balance. When a country consumes more than it produces and finances the gap through capital inflows, it runs a trade deficit. Tariffs do not close that gap unless they fundamentally alter domestic savings or fiscal deficits. The deficit is mostly a macro story, and tariffs are a micro tool.

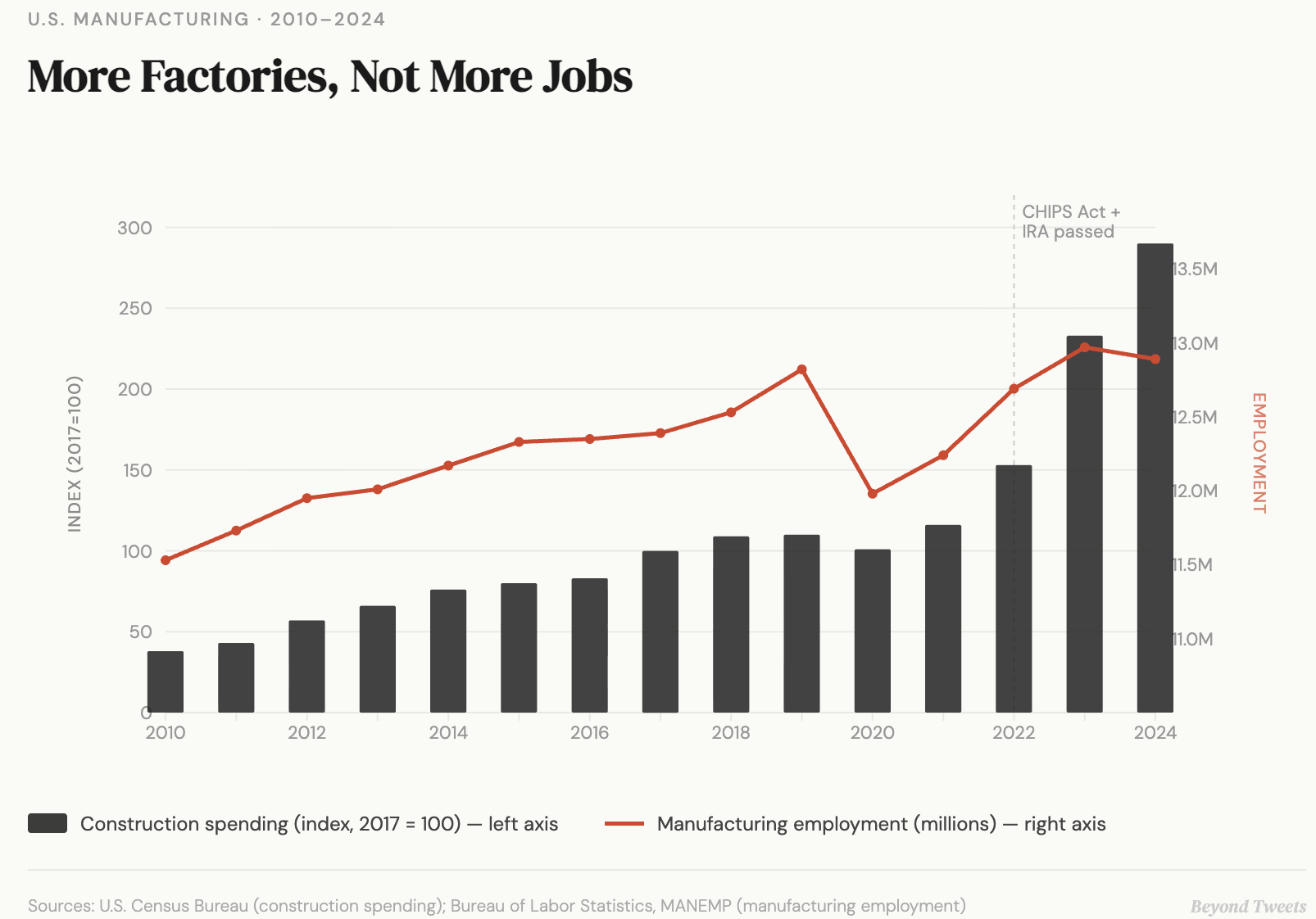

Manufacturing and Jobs: Capacity Up, Employment Flat

The second scoreboard is domestic industry. Did tariffs bring back manufacturing?

The answer depends entirely on what you look at.

There has been a genuine surge in announced manufacturing investment in the United States, especially in semiconductors, batteries, and advanced manufacturing. Factory construction spending has risen sharply. New facilities are going up at a pace not seen in decades. But that wave is driven largely by targeted industrial policy and subsidies: tariffs are part of the backdrop, not the primary engine. I wrote about this Capex boom a couple weeks ago.

Manufacturing employment tells a more sobering story. After a brief post-pandemic rebound, job growth slowed again. Factories actually shed roughly 108,000 jobs in 2025, even as tariff rates were at their highest in decades. Employment levels remain well below early-2000s peaks. Automation, capital intensity, and productivity gains mean new factories do not necessarily translate into large numbers of jobs.

Tariffs can protect specific producers while raising costs for others. There are genuine examples where they helped. There are also examples where consumers paid significantly more for modest job gains. Tariffs are an expensive way to buy time, and whether that time gets used productively is a separate question entirely, one the tariff itself cannot answer.

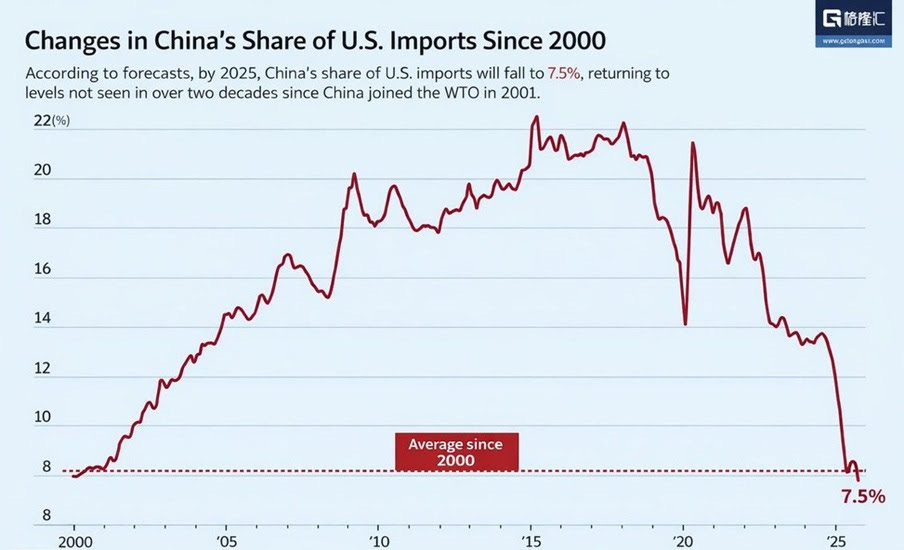

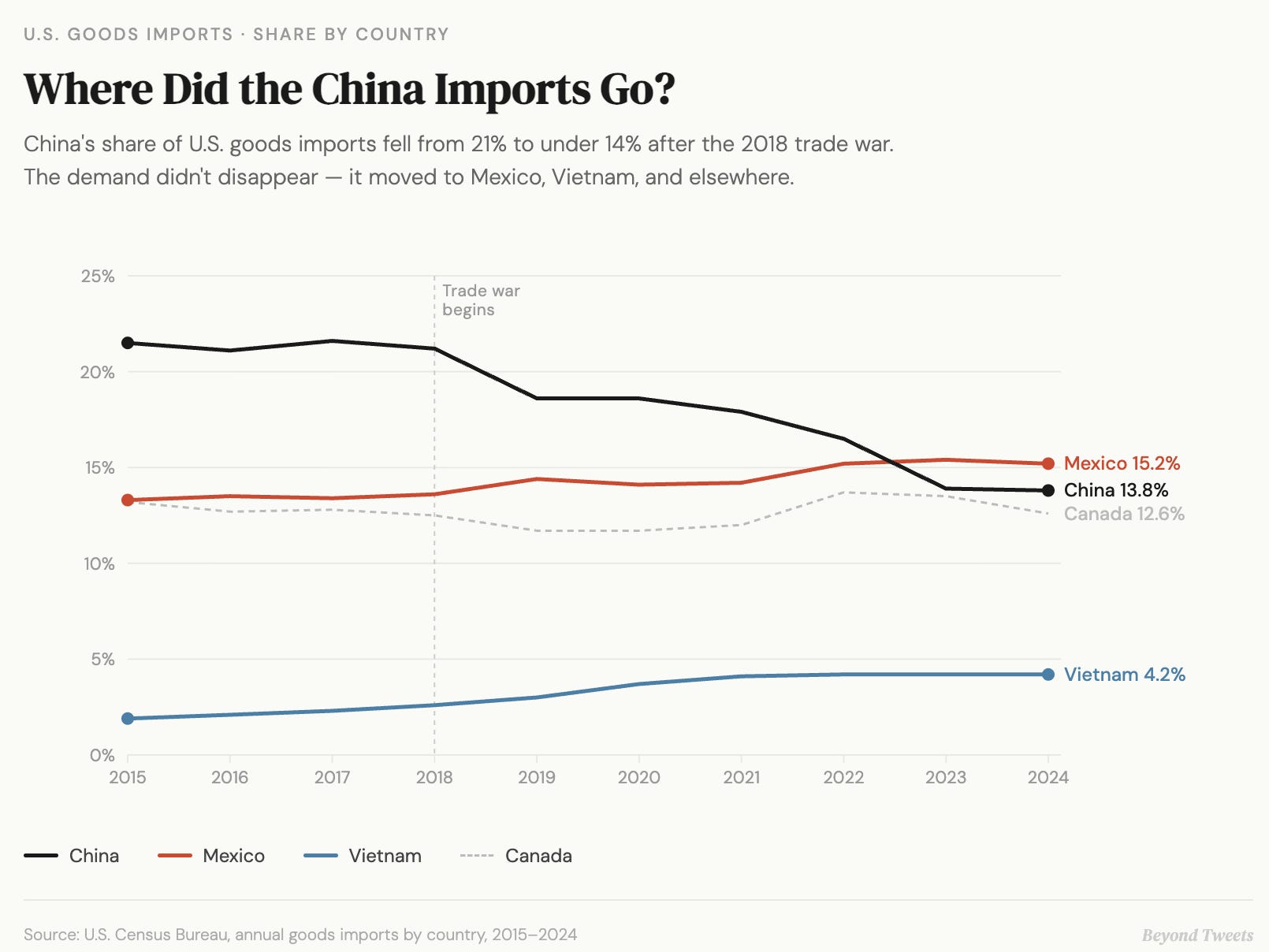

Strategic Decoupling: Less China, More Geography

The third scoreboard is strategic. Have tariffs reduced dependence on China?

Here the answer is clearest.

China’s share of U.S. imports has declined materially. Supply chains have diversified. Firms increasingly design production systems with geopolitical risk in mind, that shift is real. But it is not the same as reshoring. Much of the movement has gone toward “friend-shoring” or nearshoring: Mexico, Southeast Asia, India. Geography changed. The fundamental import dependency did not collapse.

Mexico became the largest U.S. trading partner by total volume. Vietnam’s trade surplus with the U.S. surged. Tariffs are effective at changing who you buy from. They are much weaker at changing how much you buy from abroad. So if your scoreboard is “smaller China deficit,” you can claim progress. If your scoreboard is “smaller total deficit,” the result looks like a stalemate.

And both readings are technically defensible, because they’re measuring different things.

There is also the rerouting problem. When tariffs target one country, goods often flow through intermediaries. Assembly moves. Final processing relocates. Ownership structures shift. Some Chinese content still reaches U.S. markets indirectly. If you’ve ever watched a procurement team respond to a cost shock, you know how fast they can re-map a supply chain on paper.

Strategically, diversification itself may be the objective — and on that specific metric, tariffs combined with corporate risk management have nudged supply chains toward greater dispersion. The tradeoff is cost and complexity. Diversified supply chains are often more resilient but also less efficient, and companies are explicitly accepting that tradeoff because geopolitical risk is now priced differently than it was a decade ago. The calculation changed, not just the tariff.

The Deals America Didn’t Make

There’s a cost to tariffs that doesn’t show up in any of the three scoreboards.

In January 2026, the EU and India concluded what both sides called the “mother of all deals”: a free trade agreement nearly two decades in the making, covering two billion people and roughly 25% of global GDP. The timing wasn’t coincidental: the US had imposed combined tariffs of up to 50% on Indian goods, including penalties targeting India’s purchases of Russian oil. New Delhi looked at that and decided it needed a hedge. Brussels, bruised by steel tariffs and a widespread sense of betrayal, had the same instinct.

The deal that took eighteen years to negotiate crossed the finish line in months once the incentive became obvious enough.

Canada moved in a similar direction. Prime Minister Carney flew to Beijing, met with Xi Jinping, and agreed to lower tariffs on Chinese electric vehicles and canola oil, unlocking what Ottawa framed as $7 billion in export markets for Canadian farmers. Canada also relaunched trade negotiations with India, signed a new agreement with Indonesia, and announced intentions to pursue deals with ASEAN and Mercosur. Carney explicitly vowed to double Canada’s non-US exports. That’s not a trade policy adjustment. That’s a structural pivot driven almost entirely by the unpredictability of Washington.

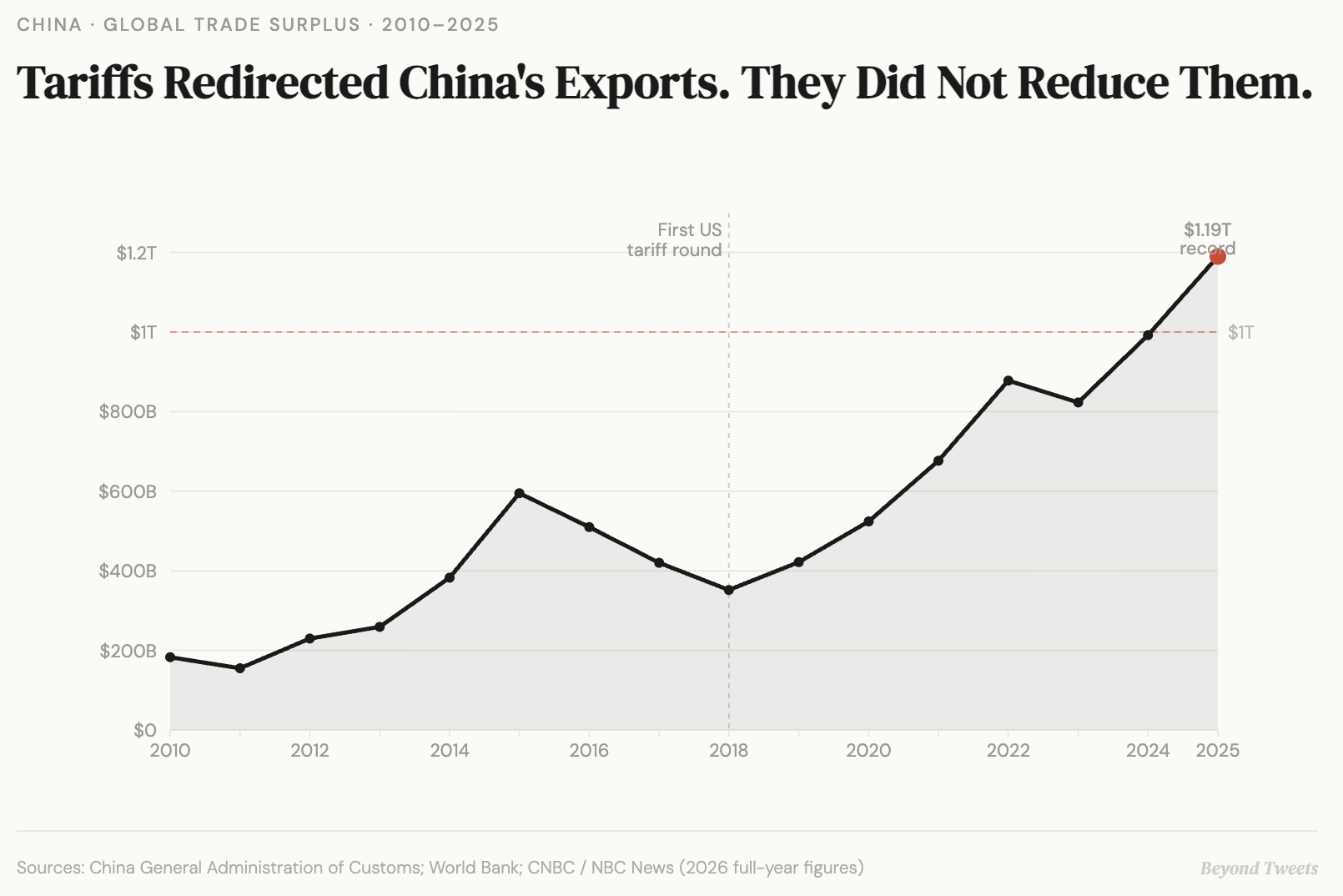

What the US tariff strategy has accomplished, in part, is to accelerate the formation of trade relationships that exclude it. China has been the quiet beneficiary: its trade surplus hit a record $1.1 trillion in 2025 despite US tariffs, as countries pushed out of the American orbit found other buyers and sellers willing to engage without conditions.

Last week’s Supreme Court ruling is a useful illustration of how durable this logic becomes. The IEEPA tariffs were struck down on Thursday. By Friday evening, a replacement 10% global tariff was already signed under a different authority, now raised to 15%, with a 150-day clock that expires just before the midterm elections.

What’s really happening, I think, is that the world is repricing risk. The era of treating supply chain efficiency as the only variable worth optimizing is over. The irony is that America’s trading partners ran the same calculation Washington did. They looked at the uncertainty, priced it in, and started diversifying. The US pushed them to behave exactly as it said it wanted to behave. They just didn’t do it with the US.

What Tariffs Are Actually For

There is one case where the logic holds more cleanly, and it’s worth naming before we close.

Both the US and the EU have imposed targeted tariffs on Chinese electric vehicles: the US at 100%, the EU at up to 35.3% on top of an existing 10% duty, following a formal anti-subsidy investigation. The stated rationale in both cases is Chinese state subsidies flooding the market with artificially cheap exports. But the real logic running underneath that is something simpler: Chinese EVs are genuinely better and dramatically cheaper than what Western manufacturers currently produce, and the gap is structural, not temporary.

BYD sells EVs in Europe starting around €10,000. The average Chinese EV entering Europe is priced at less than half the average EU-made equivalent. China sold 12.87 million EVs domestically in 2024, accounting for 41% of all new car sales. It exported roughly 6.5 million vehicles in 2025, overtaking Japan to become the world’s largest car exporter. The China Passenger Car Association expects that number to reach 10 million by 2030.

Western producers are not losing on subsidies. They’re losing on a decade of integrated industrial policy (i.e. battery supply chains, raw material access, manufacturing scale, and software iteration) that simply cannot be replicated overnight. The tariffs aren’t fixing that gap. What they’re doing is buying time for local producers to figure out whether they can close it at all.

This is the most defensible version of the tariff argument: not that they change the underlying economics, but that they slow the clock enough to allow domestic adjustment. The EU’s approach at least acknowledges this honestly: the Commission framed the duties explicitly as a temporary measure to “level the playing field,” not a permanent wall. Whether Volkswagen and Stellantis can actually use that time productively is a different question. But the intent is coherent. You don’t need the patient to be cured immediately. You need the hospital to stay open while treatment is figured out.

The problem is that this logic applies cleanly only when the protected industry has a credible path to competitiveness, and only when the tariff is specific, time-limited, and paired with something else: investment, R&D, industrial strategy. When it’s broad, permanent, and applied to everything from steel to canola oil, “buying time” becomes something harder to distinguish from avoidance.

What Tariffs Actually Buy

So are tariffs working?

The honest answer is: it depends on which problem you started with.

For reducing bilateral exposure to China, yes, partially. For permanently shrinking the overall trade deficit, no: the 2025 data makes that case as clearly as any argument could. For catalyzing strategic domestic capacity in select sectors, sometimes, and usually only when combined with subsidies and industrial policy that do the actual heavy lifting.

What I keep coming back to is the time problem. Tariffs can buy time. They can make a structural transition slightly more manageable, slowing import penetration in a sector while domestic alternatives develop, or making offshoring less automatic. That is a real function. But the time purchased by a tariff is only as valuable as what gets built during it.

A protected industry that uses the window to become more competitive is a different story than one that uses it to lobby for more protection.

That distinction, between tariffs as a bridge and tariffs as a destination, is what the scoreboard debate almost never discusses. The Supreme Court ruling reshuffled the legal deck last week, but it didn’t change the underlying question. The next 150 days will tell us a lot about which kind of story this turns out to be.

Have a great weekend!

Giovanni