I Was Right!

#191 - Reality check on some (self selected!) predictions

A few weeks ago I stumbled on this tweet. It was one of those posts that stops your scroll because the numbers feel wrong, even when they’re right. The line was simple: “A weekly jab in the belly is generating more revenue than the entire AI industry. Ozempic + Mounjaro.” My reaction was: I was right!

Not that exact line, obviously. But in May 2024, I wrote a post titled “Bigger than AI” (2 years ago!), a post where I argued that GLP-1 drugs would be more transformational for society than artificial intelligence. At the time, it felt like a stretch. AI was eating the world. Everyone I knew was talking about GPT-4, about prompting, about which jobs would disappear first. And I was writing about weight loss injections.

So this is a reality check. Not a victory lap. I’m one observer among millions, and the trends I flagged were hiding in plain sight for anyone willing to look sideways. But there’s something worth doing in going back to your own predictions and asking honestly: did reality cooperate?

Before diving in, I’ll admit up front that there’s a post coming on the calls I got wrong, I’m working on it, and there’s plenty to own up to. This isn’t that post. I picked these three predictions because I keep thinking about them.

Every time I write about a topic I do my homework, hit publish and my phone lights up: friends send links, my feed serves up new papers and stories. Sometimes I curse myself for leaving out a great detail; other times I’m just glad I have an excuse to keep learning. This round‑up gathers those updates in one place. It isn’t a victory lap. It’s a chance to check in on how these stories have evolved and to celebrate what we’ve learned.

Act I: The Jab Heard Round the World

In “Bigger than AI,” I cited a Barclays analyst named Emily Field who said that if you wanted a comparison for GLP-1 drugs, you had to look at the invention of the smartphone. At the time, 9 million Americans had an Ozempic prescription in a single quarter. 47% of American adults said they wanted to try these drugs. I called it the most important health technology of the decade and argued it would reshape industries far beyond pharma: food, insurance, fitness, fashion, urban planning.

Two years later, 30 million Americans are on GLP-1 medications. The market went from $6 billion in 2023 to a trajectory that Goldman Sachs projects will hit $100 billion by 2030. Morgan Stanley puts it at $190 billion by 2035. The FDA approved the first oral Wegovy pill in December 2025, which means we’re moving from weekly injections to something you take with breakfast. The implications of that shift alone could fill another post.

What I find most interesting isn’t the growth itself. Lots of things grow. It’s that the framing has quietly shifted. In 2024, calling GLP-1s “bigger than AI” sounded like provocation. Now investment banks are publishing reports with titles like “Weight Loss Drugs: A Revolution Bigger than AI?” and nobody blinks. The Overton window moved. The argument I made isn’t contrarian anymore. It’s consensus.

I did a mid-year check in “What Did I Get Right (And Wrong)?” (#90) and wrote that I was, if possible, more bullish than ever. I still am. Not because the revenue numbers are impressive, though they are, but because we’re watching a technology that changes the physical reality of hundreds of millions of people. AI changes how we work. GLP-1s change how we live in our bodies. Both matter. But only one of them makes your doctor rethink everything she knows about cardiovascular disease, diabetes, addiction, and possibly Alzheimer’s.

And then there’s the argument that reframes almost everything. Someone pointed out something that should haunt public health officials: COVID wasn’t primarily a disease of the old. It was a disease of the metabolically unhealthy. Japan in 2020 was the oldest country on Earth, with nearly 29% of its population over 65. The US had only 17%. By every demographic measure, Japan should have been devastated. Instead, Japan lost 126 people per million. The United States lost 1,965. The country with nearly double the share of elderly suffered one seventeenth the death rate. The difference wasn’t age, wasn’t masks, wasn’t culture. Japan’s obesity rate was around 4%. America’s was above 40%.

Follow that logic forward and the GLP-1 story stops being about revenue or even individual health. Tirzepatide produces roughly 20% average weight loss. Semaglutide reduces major cardiovascular events by 20% independent of weight loss. Systemic inflammation falls. Diabetes reverses. If COVID had arrived in 2030 instead of 2020, with the majority of at-risk Americans on these drugs, the US would have entered the pandemic with roughly the metabolic profile Japan had a decade earlier. The death toll, by this estimate, would have dropped from 1.2 million to somewhere between 100,000 and 200,000.

I’m genuinely surprised by the steady stream of good news about GLP‑1 drugs. New results from Eli Lilly’s TRIUMPH‑1 trial show that retatrutide, a weekly shot that works on three hormones, helped people lose about 28 percent of their body weight in 80 weeks; nearly half of participants lost at least 30 percent and those with severe obesity who stayed on the highest dose for two years shed roughly 30 percent (an average of 85 pounds).

Beyond weight, retatrutide trimmed waistlines by around nine inches and improved cholesterol, triglycerides, blood pressure and inflammatory markers. Other GLP‑1 drugs are proving versatile: semaglutide cut the risk of major cardiovascular events by around 20 percent in the SELECT trial, and researchers estimate that roughly two‑thirds of that benefit comes from direct effects on the heart and blood vessels rather than weight loss.

These medicines are also being tested or approved for sleep apnea, fatty liver disease, chronic kidney disease and heart failure. The cancer data is even more unexpected. A large Penn Medicine study presented at the 2026 ASCO meeting found women taking GLP‑1 drugs were about 30 percent less likely to develop breast cancer and showed similar results in a matched cohort. Another study of more than 137 000 breast cancer patients reported that roughly 96 percent of women who used GLP‑1s were alive five years after surgery, compared with about 90 percent of non‑users. These signals are from observational research, and clinical trials are needed to confirm them, but they hint at broader benefits: GLP‑1 drugs may reduce cancer risk and improve survival.

The tweet that started this post was right. A weekly jab in the belly is generating more revenue than the entire AI industry. Sometimes the biggest disruptions don’t look like disruptions. They look like medicine.

And as many people argue: we might be at a point in history where obesity is a problem of the past. And this might be one of the most important scientific results in many decades.

Act II: The Continent Nobody Was Watching

In January 2026, I published “2026: The Year of Reasonable Optimism” (#171), where I argued that the EU was entering an unexpected moment of strength. The thesis was counterintuitive, bordering on unfashionable: in a world tilting toward extremes, stability, predictability, and rule-based coordination were becoming undervalued assets. Europe, I wrote, might be the boring bet that outperforms.

I want to be careful here, because “Europe is back” is a headline that has been written and retracted so many times it’s practically a genre. But something is genuinely different this time, and the data is starting to pile up in ways that are hard to dismiss.

A few weeks ago, a researcher named Ben Bawan posted a chart showing that for the first time in recorded history, more Americans are moving to EU, EFTA, and UK countries each year than Europeans from those places are moving to the United States. The ratio was 4:1 in favor of the US in the early 2000s. It crossed parity around 2022. Now it’s reversed. People vote with their feet, and feet are walking eastward across the Atlantic.

Bawan posted another chart that really got me jumping on my chair (I tried to express this excitement to my kids while on a family vacation and that ended up being a family joke… everyone at home mocks me for getting excited for shit nobody cares about!) : if current demographic trends hold, Europe may soon record more live births than all of China. That would be the first time since the Qing dynasty, possibly the first time in history. Ain’t that unbelievable?

Meanwhile, on the policy side, things moved faster than I expected. EU defense spending hit 21% of the global total. The bloc committed €800 billion in additional defense spending through 2030. The EU-Mercosur trade deal that I discussed in “A Good Week for EU” (#154) is moving forward. And back in that September 2025 post, I highlighted ASML’s €1.3 billion investment in Mistral and Bending Spoons buying Vimeo for $1.38 billion as signs that European tech was growing real muscle.

Did Europe suddenly become a superpower? No. Is the bureaucracy still maddening? Absolutely. But the gap between perception and reality has widened to the point where the perception itself is becoming a mispricing. Investors, talent, and governments are slowly noticing. When Draghi said Europe risked becoming “a marginal player, dependent on allies and vulnerable to rivals,” it landed like a diagnosis. The treatment, for once, seems to have started.

I just started reading Alec Ross’s book The Italian Dream, and the introduction landed at exactly the right moment. Ross makes a point that feels obvious once you read it, but I’d never framed it this cleanly: we Europeans are catastrophically bad at branding the model we’re building. Look at the metrics objectively. Life expectancy, quality of life, social mobility, work-life balance, infant mortality, income inequality: the EU leads, or closely matches, virtually every comparable measure against the US and China. And yet the global imagination is still structured around “the American Dream” and, increasingly, “the Chinese Dream” or “the Indian Dream.” There is no European Dream that anyone talks about. There is no Italian Dream. Ross’s argument is partly linguistic: in Italian, calling someone a sognatore is almost an insult, a dreamer with his head in the clouds, while in English or Mandarin “visionary” means someone who shapes the future… but the deeper point is cultural. A civilization that produces exceptional outcomes but refuses to narrate them is leaving influence on the table.

The migration data I cited above is people discovering the European model empirically, because Europe never bothered to advertise it. The gap between what Europe actually delivers and what the world thinks it delivers is a branding problem. And branding problems, at least, are solvable.

Act III: The War You Can’t See

In June 2025, I published “Electrone War” (#139), arguing that the real test of AI leadership wasn’t chips or code. It was electricity. The country that could generate, store and deliver the most electrons at the cheapest price would win the AI race, and probably the broader industrial competition along with it.

The numbers then were already striking. AI and data centers were projected to become a meaningful share of electricity demand, while power grids in many Western countries were struggling with permitting delays, aging infrastructure and long interconnection queues.

A year later, the picture has become sharper.

Goldman Sachs now estimates that U.S. data-center power demand will rise from 31 gigawatts in 2025 to 66 gigawatts in 2027, more than doubling in just two years. The International Energy Agency expects global data-center electricity consumption to roughly double by 2030, reaching around 945 TWh. China and the United States alone are expected to account for nearly 80% of that growth.

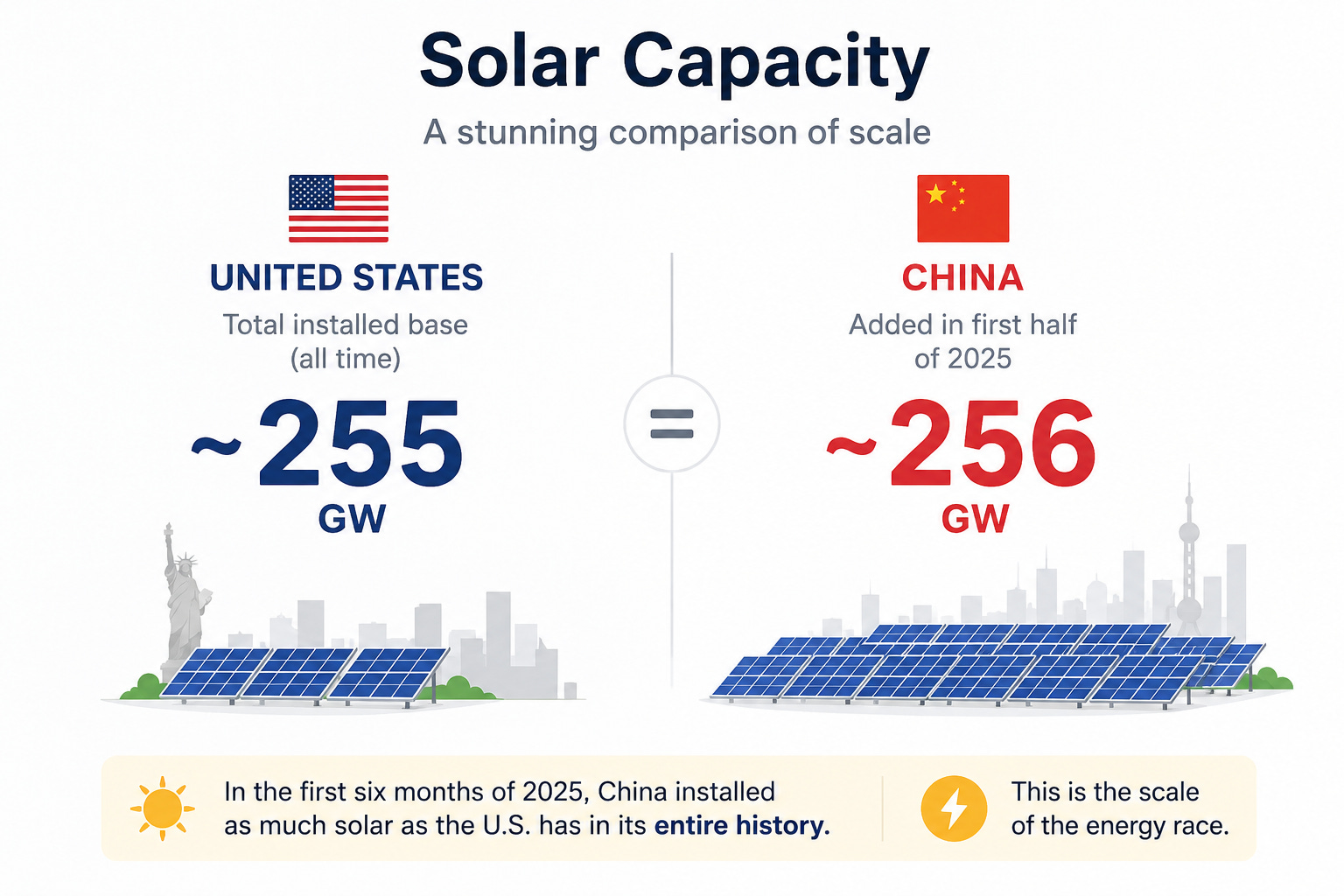

What caught my attention most, however, was a statistic that has little to do with AI directly. In the first six months of 2025, China installed roughly 256 GW of solar capacity. That’s approximately the same amount of solar capacity that the United States has installed in its entire history.

The reason I find this comparison useful is that it illustrates the scale at which China is building energy infrastructure. The discussion around AI often focuses on models, chips and export controls. Those matter. But all of those technologies ultimately depend on abundant and reliable electricity.

This is the prediction I feel most strongly about, and it’s the one that gets the least attention. The AI discourse is consumed by model benchmarks, chip export controls and which lab released what. Those things matter. But they matter the way the engine matters in a car that has no fuel. You can build the most sophisticated AI infrastructure on Earth, and it’s worth very little if you can’t power it affordably and reliably.

The editorial plan for this newsletter includes a full sequel called “China Won the Electrons War” (it’s already outlined), so I won’t exhaust the argument here. But the short version is this: while the U.S. celebrates progress in models and chips, China continues to expand the energy infrastructure that makes everything else run. The scoreboard everyone watches isn’t necessarily the one that determines the outcome.

And Europe? The energy picture there remains a separate kind of painful. Stopping nuclear in Germany, underinvesting in grid interconnection and fragmenting energy policy across 27 national regulators. The Electrone War post already flagged this, and nothing since has made it look better.

The Scoreboard Nobody Asked For

Three predictions. Three reality checks and (hopefully) interesting follow-ups.

GLP-1s bigger than AI: confirmed, and accelerating. The market data, the clinical pipeline, the oral formulations all point in the same direction. This one is no longer a prediction but rather an observation.

EU renaissance: directionally right, magnitude uncertain. The structural indicators are real, the policy shifts are meaningful, the migration and birth data is genuinely surprising. But Europe has a long history of almost-moments that stall. I’ll keep watching.

The Electrone War: the thesis is stronger than when I wrote it. China’s energy buildout is not slowing down, US grid bottlenecks are not resolving, and the disconnect between the AI hype cycle and energy reality is growing. This one worries me the most, because unlike GLP-1s or EU policy, this is a hard constraint to overcome.

What do these three predictions have in common? None of them were about technology itself but they were about the infrastructure underneath technology: the biological infrastructure of human health, the institutional infrastructure of trade and governance, the physical infrastructure of energy.

The lesson, if there is one, is boring: the substrate matters more than the surface. The pipes matter more than what flows through them.

I don’t say this to claim foresight. Most of the people I cited in those original posts saw these trends before I did. I just happened to write them down in a newsletter and connect a few dots that were already visible. The real question isn’t whether these predictions were right. It’s what they suggest about the next set of questions we should be asking.

But that’s a post for another week.

Have a great weekend!

Giovanni