ZIRP: The Age of Hyper-Growth

ZIRP: The Age of Hyper-Growth

#30 - Unpacking the Zero Interest Rate Phenomena

In case you prefer to read this post in Italian check out the translations ChatGPT wrote for me.

Hello friends, I hope you’re having a great Sunday!

Today I’d like to write about how in the last years the macroeconomic situation and the bullish markets pushed and fostered a lot of innovation but also a lot of capital going into business models that had fundamental flaws. Most people refer to these companies and market segments as “ZIRP” (Zero Interest Rate Phenomenon). The basic assumption is that these companies thrived in a bullish market, where money was “free” (or very cheap) and abundant and where growth was really the only thing that mattered. I already wrote about this “alpha vs beta companies” a few months ago, I feel like this is a very interesting change happening in the industry and I am spending quite some time thinking about this and its implications. Today I would like to unpack a bit these “ZIRPs” and potentially see if there’s anything for us all to learn. I hope you like it!

The inspiration for this post came from this tweet I randomly stumbled upon:

Not something particularly insightful but since I have always been a big fan of the subscription boxes ideas it’s something that caught my attention. I then stumbled upon this article that was commenting the struggle that Getir (the instant delivery company that at its peak raised $1.8B from top investors) is going through as they rationalise the business and close some segments. And then I read a piece that was commenting how “Uber and Lyft both trade well below their IPO prices and have collectively reported $43B in losses since their inception. In Lyft’s case, shares have lost 88% of their value since their first trading day in 2019, with a chink of that loss coming last week when the founder stepped down and the new CEO said the company is not for sale”.

Subscription boxes, instant ecommerce delivery and ride sharing apps apparently do not have a lot in common. But I think they all actually belong to this definition of the “Zero Interest Rate Phenomenon” that flourished in the past few years in an unprecedented macroeconomic environment. This condition was largely a consequence of the global financial crisis and the ongoing COVID-19 pandemic, which both prompted central banks worldwide to lower their interest rates in an attempt to stimulate economic growth. In some cases, these interest rates have even turned negative, an unconventional policy measure intended to discourage banks from holding onto reserves and encourage them to lend more to businesses and consumers.

This low-to-zero interest rate environment significantly impacted the world of venture capital (VC). Traditionally, venture capitalists have sought high returns by investing in early-stage companies with high growth potential. With interest rates at historic lows, the cost of borrowing decreased dramatically. This meant that venture capitalists had access to cheap capital, allowing them to finance more startups and take bigger risks. Simultaneously, institutional investors and high-net-worth individuals, seeking better returns than those offered by traditional assets such as bonds, began to funnel more money into venture capital funds.

The resulting flood of capital into the venture capital space gave rise to a myriad of companies with debatable unit-economic financials, and business models that would burn cash at tremendous speed. These companies were able to raise large amounts of capital, often at high valuations, and use it to scale quickly, capture market share, and disrupt traditional industries - even if their business models were not yet profitable.

How and when did things change?

Over the last few quarters, after the “Covid hangover”, a notable shift has begun to emerge in the macroeconomic landscape. Central banks worldwide are starting to respond to inflationary pressures by increasing interest rates. This change comes after years of low-to-zero interest rates, a policy that was crucial in maintaining economic stability and growth during periods of significant upheaval, such as the global financial crisis and the COVID-19 pandemic. However, as the global economy begins to recover, the low interest rate environment is starting to reverse, creating a ripple effect in the venture capital space and the segments it has heavily influenced.

The venture capital world, which had been reveling in the era of cheap capital, is beginning to feel the impact of this shift. The cost of borrowing is rising, making it more expensive for VCs to fund new startups and for startups to sustain their operations, particularly those with high burn rates and unprofitable business models. This change is prompting a reevaluation of the "growth at all costs" mentality that dominated the zero-interest rate era. Investors are becoming more cautious and discerning, prioritising profitability and sustainable growth over rapid expansion.

The segments heavily backed by venture capital during the zero-interest rate era - I picked my favorite in the coming paragraphs - are feeling the brunt of this transition. For instance and as I wrote in my previous post, D2C companies, which often operate on thin margins and rely heavily on customer acquisition, may find it harder to secure funding as investors become more risk-averse. Similarly, scooter companies, which require significant upfront capital expenditure and have struggled with profitability, could face hurdles in securing further funding.

While this is a very dire situation for most of these companies, I do not believe the conclusion is that these businesses were a total fade and that history is going to forget about the ZIRP madness. I believe that as in most economic revolutions most of the fundamental customers demand changes are here to stay, but in those segments some incumbents adjusted and recovered some of the lost ground, in other segments some of the startups are going to consolidate their position through acquisition often at interesting entry prices (e.g. Getir buying Gorillas for $1B, a fraction of the peak valuation). In some other cases the ZIRP companies will manage to pivot, strengthen their financials and business models and eventually build sustainable long-term businesses (I personally believe that for instance Uber is doing just that, and in a very good way, building long term value).

We have seen this happening many times, and already at least twice (2001 and 2008) in the digital world: companies that adapt to the new environment, by demonstrating profitability, managing their burn rates, and delivering real value to their customers, will be better positioned to thrive in the post-zero-interest rate era. This is how FAANG (Facebook, Apple, Amazon, Netflix, Google) were born after all.

My favorite ZIRP examples

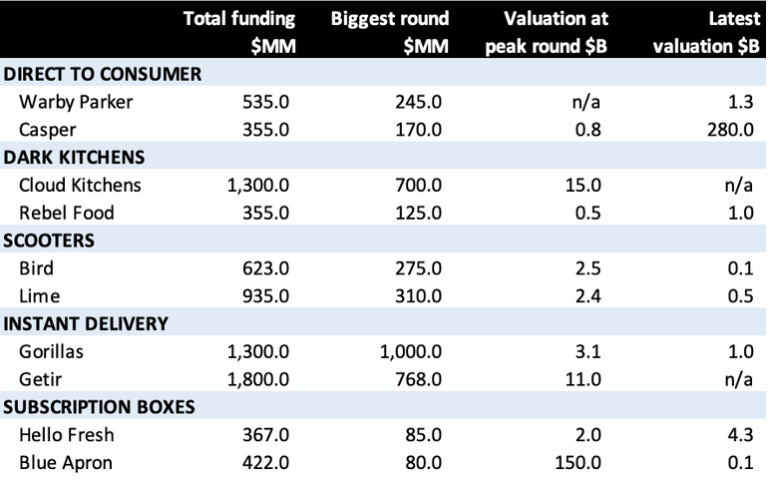

I pulled some example of segments and companies I personally consider, at least in part, Zero Interest Rate Phenomena. This is obviously just a personal consideration, and I very openly admit that I was 100% part of that “enthusiasm” during the bull market and did not at all consider most of these “ZIRP”. I looked, and in some cases participated, to the frenzy with a lot of interest and excitement. I however now, out of the center of the storm, consider how we all have collectively been blind to some clear signals and how indeed some of these segments were “too good to be true”. I filled a quick table with some key numbers to show the point, picking some of the companies I followed more closely (fact-checking disclaimer: most of numbers come from ChatGPT or quick googling, do not over-rely on them and let’s focus on the trend rather than absolute number for the sake of the narrative!).

Direct-to-Consumer (D2C)

I have largely written about D2C: in the past years as venture capital poured in, companies could afford to heavily invest in online marketing, customer acquisition, and brand building. The low cost of capital allowed businesses to prioritize growth over profitability, often offering products at lower margins. Examples include Warby Parker and Casper. Both these D2C brands managed to disrupt their respective markets (eyewear and mattresses) with the help of VC funding, allowing them to aggressively market and scale their operations. As the market got more concentrated, and capital became more scarce, this space showed a lot of the fundamental issues.

Dark Kitchens

The rise of dark kitchens, also known as ghost kitchens, which focus on delivery rather than dine-in services, require less capital for real estate and staffing. Low cost of capital and the rush to food delivery boosted by the pandemic demand shift made these models look like the “future of dining”. Examples include CloudKitchens and Rebel Foods. Both companies heavily leveraged the capital available to set up numerous kitchens across various locations, thus rapidly scaling their business.

Scooters

The micro-mobility and scooter sector, particularly e-scooters, has seen significant growth due to the zero-interest rate phenomena. The availability of cheap capital allowed these companies to flood cities with scooters before achieving profitability, focusing on rapid market capture. Bird and Lime are two examples of e-scooter companies that have benefitted from this trend. With the help of massive VC funding, they have expanded to multiple cities globally without ever becoming profitable. This sector also saw a bikes and electric bikes wave, with a model that required super expensive equipment (bikes, scooters) with high maintenance that required massive life to justify an economic profit.

Instant Delivery

While in my opinion electric scooters are the poster children of the ZIRP companies, this has probably been the apex of the trend. In the past 3 years there was a massive race to the bottom in delivery times for grocery products. Startups were flush with cash, enabling them to build extensive local delivery networks and offer services at very low prices or even at a loss. Gorillas and Getir are two examples of such businesses. These companies used the available capital to scale rapidly, offering ultra-fast delivery times in various cities across the globe.

Subscription Boxes

The subscription box market has was basically born in the zero interest rate environment. Companies in this sector used the readily available capital to offer a wide variety of products and flexible subscription plans, often at low profitability, arguing to be in the middle of a food purchase revolution. These companies were always attractive as the TAM (Total Addressable Market) is probably one of the largest, we all spend a high share of our wallets in food. Birchbox and Blue Apron are examples of subscription box companies that leveraged this trend. Both companies used the capital to acquire customers and scale their operations before turning a profit.

Drones, Action Cameras, VR and Web 3.0 (?)

I consider the caveat I made earlier, that most of these sectors and companies are not entirely scams but that they lived a super fast development that inevitably led to a misallocation of capital and super material losses. There are however some sectors where I still have not made up my mind on whether the revolution promised will simply never happen because the sectors were misunderstood, or whether these sectors are still nascent and we still have not understood the full potential.

For instance the Drones industry was born and grew exponentially in the past 10 years, there was a lot of VC funding going into companies like DJI and Zipline, that spent a lot of money in R&D and product development. However the demand was probably weaker than in most optimistic forecasts (how many people do you know that really use a drone regularly?) and the regulatory landscape probably harder than imagined. While the industry has some super relevant applications, for instance in the defense industry, I personally believe that the promise of the consumer drones market was inflated. Similar considerations could be made for action cameras (we all got a Go Pro, until we realized the last thing we wanted to do was to watch 5 hours of raw footing of us skiing, badly) or VR headsets, on which I wrote a post a few weeks ago.

The one sector I consider most controversial is Web 3.0. This sector did indeed receive an unprecedented, probably in capitalism history, inflow of capital and attention. And arguably this blessing was its curse. The industry of decentralized, blockchain-based applications benefitted a lot from the availability of cheap capital which allowed for significant investment in the development and marketing of these applications, despite their nascent stage and uncertain regulatory status. Companies like Coinbase or the infamous FTX raised tens of billions, promising to be revolutionising finance. And while I still believe the fundamentals are incredibly promising, and that Web 3.0 will indeed have a material impact on our economy in the coming decades, we can say that at today at least a portion of the “revolution promise” was missed.

Why did we all get “crazy”?

The key learning is that “Unit economics”, which refer to the direct revenues and costs associated with a business model on a per-unit basis, can often be diminshed in importance in a booming environment characterised by low interest rates and ample venture capital funding. There are several reasons why this happens:

Focus on Growth Over Profitability: When there's an abundance of capital available at low cost, startups can afford to prioritize growth over immediate profitability. They can use the capital to invest heavily in marketing, sales, and customer acquisition, even if it means making a loss on each unit in the short term. The goal is to capture as much market share as possible and achieve economies of scale, which should eventually lead to positive unit economics.

Investor Expectations: In a booming environment, investors are often more interested in growth potential than current profitability. They're willing to invest in companies with negative unit economics if they believe those companies can grow quickly and dominate their markets. This encourages startups to focus on growth metrics like user acquisition and revenue growth, rather than on unit economics.

Competitive Pressure: If competitors are raising large amounts of capital and growing rapidly, startups may feel pressured to do the same in order to keep up. They may choose to invest heavily in customer acquisition and retention, even at the expense of unit economics, to prevent competitors from capturing their market share.

Future Profitability: Startups often argue that they can improve their unit economics in the future once they've achieved scale. For example, they may be able to negotiate better terms with suppliers, improve operational efficiency, or increase prices. This argument can convince investors to overlook negative unit economics in the short term.

Execution always wins, in the long run

In a booming economy characterized by ample capital and strong market potential, it can be tempting for managers and founders to ride the wave and prioritize growth above all else. However, it's crucial to maintain a keen focus on execution and key business fundamentals, such as operating margin and unit economics.

Going back to the intent of the post (i.e. not laugh at common mistakes, that I certainly did, in evaluating some models but rather try to learn something from our recent past) I tried to sum up some of the key insights I noted when reflecting on the topic. Most of the points below are very intuitive, not so smart and things that should be common knowledge for most of people operating in business contexts. However since I, for first, decided to “ignore” them or pretend they were not true anymore in “the new economy” I believe it’s not a bad idea to quickly write them down.

Lesson #1: understand your business (i.e. you can’t optimize what you don’t measure or understand)

Understand Your Unit Economics: Regardless of the external environment, understanding your unit economics is vital. This involves knowing the cost to acquire a customer (CAC), the lifetime value of a customer (LTV), and the margin made on each unit sold. These metrics provide insight into your business's profitability potential.

Prioritize Operational Efficiency: Efficiency in operations directly impacts your operating margin. Lean operations, streamlined processes, and a culture of continuous improvement can help maintain profitability even as you scale.

Monitor Key Metrics: Beyond just revenues and user growth, monitor metrics like customer retention, customer satisfaction, and cash flow. These can give you a more holistic view of business health.

Sustainable Growth: While rapid growth can be exciting, it's important to grow at a pace that your business can sustain. This often means finding the right balance between acquiring new customers and retaining existing ones, investing in expansion and maintaining cash reserves, and pushing for market share while keeping an eye on profitability.

Lesson #2: Staying Afloat in a Downturn Economy

On top of keeping the bar straight in booming times, I also think that the current situation taught us that survival skills are really important once “shit hits the fan”. The last years have showed us how, both in business and life as Rifkin argues in his latest book, the key skill on top of efficiency is resilience: you need to stay alive to ride the next bull wave! Here are some key areas that help staying resilient:

Cost Management: In a downturn, maintaining a healthy operating margin becomes even more critical. This may involve cutting non-essential expenses, renegotiating contracts with suppliers, or finding more cost-effective ways to operate.

Preserve Cash: Cash is king, especially in a downturn. This might mean delaying expansion plans, reducing inventory, or improving collections processes to preserve cash.

Focus on Core Customers: In tough times, it's crucial to focus on retaining your most loyal and profitable customers. They can provide a steady source of revenue and can be more cost-effective to serve than acquiring new customers.

Adapt and Innovate: Downturns often require businesses to pivot or adapt their business models. This could involve finding new revenue streams, entering new markets, or offering new products or services that meet the changing needs of your customers.

What are the sectors or companies you believe I missed in the list above? And do you think I misunderstood any of the comments, failing to grasp how the revolution is still in the making? I hope to hear your considerations in the comments.

Wish you a fantastic Sunday and a lovely week!

Giovanni