The Coming (Robots) Wave

#193 - We're talking about models and agents, but robots might be AI future

Hello friends, I hope you had a great week!

There’s a line from Andrej Karpathy that’s been rattling around my head for a few weeks now. He was talking about the next decade of AI, and he said something like: the first wave was about language, the next wave is going to be about physical work. I’m paraphrasing, but the shape of the claim stuck with me. The first wave compounded on top of digitized text. The next one compounds on top of what you could call digitized physicality: space, motion, force, the world of atoms catching up to the world of bits.

I’ve been carrying this around partly because of how unsexy the implication is. Every AI conversation I’m in lately sounds the same. Which model. Which benchmark. Which valuation. Who’s beating whom. None of it is about the physical world. And I can’t shake the feeling that we’re debating the wrong scoreboard at exactly the moment the interesting curve is starting somewhere else entirely.

I recently wrote a post starting from a tweet that noted how AI really started in the 1990s, when we began converting the world into bits, not in 2022. The thing we now call the AI revolution was just the visible part of a thirty-year compounding curve. What I’ve been wondering lately is whether the same thing is now starting on the physical side, and whether we’re underrating it for the same reason we underrated digitization while it was happening: because the boring infrastructure phase doesn’t look like a revolution while you’re inside it.

The boundary I drew, and where it’s bending

In my previous post I argued that AI’s power is a function of how digitized a domain is. A financial analyst works in a fully digital environment, so AI compounds aggressively on top of her work. My sister, a Pilates instructor, works in a domain that’s almost entirely analog, and there’s barely any substrate for AI to compound on. The conclusion I landed on was that the boundary of AI’s impact is the physical world, the stuff that hasn’t been converted to bits.

I even joked, half-seriously, that my childhood friend who runs a gelateria in Italy was safe because the value of his business is the vibe of the place, the chat, the summer evening, the way you feel sitting outside. I wrote that maybe AI and robotics would eventually automate gelato production, but who cares, that’s not where the value lives.

That maybe is what I’ve been thinking about. The boundary I described was real, but I framed it like a wall when it was really a frontier, and frontiers move. The more I look at what’s happening on the robotics side of the AI build-out, the more I think this frontier is starting to move faster than I’d expected, because three unrelated curves have all finished their boring phase at roughly the same time.

Vision models that can finally handle the variance of a real physical environment.

Humanoid and bi-armed platforms at a price point that doesn’t kill the business case.

And cheap electrons, the thing I wrote about in the China post, which is the substrate underneath all of it.

The lights are already off in several rooms

Here’s the part that surprised me when I started looking at the actual data. I had the fully automated factory filed under 2030 predictions, and it turns out to be a 2026 operating reality, just a quiet one.

Xiaomi runs a plant in Changping, near Beijing, that produces roughly one smartphone per second with no humans on the production floor.

About ten million units a year, no shifts, no breaks, no lighting in most of the line because lighting is for human eyes. There’s a Chinese textile facility running five thousand looms around the clock with similar economics. Foxconn’s Kunshan plant displaced around sixty thousand workers over the last few years as it rolled out lights-out lines. China’s manufacturing workforce went from one hundred and fifteen million people in 2013 to roughly eighty-five million in 2025, even as exports hit record levels. That’s a thirty-million-person drop in headcount happening underneath a story of industrial dominance, and almost nobody outside the supply chain world is talking about it.

The Western side of the wave looks different but compounds in the same direction. Tesla has more than a thousand Optimus Gen 3 humanoids working in its own factories as of early 2026 and is converting the Fremont Model S and X line into a one-million-unit-per-year humanoid manufacturing facility. Figure is raising at humanoid-as-real-product valuations. Gartner expects sixty percent of manufacturers to adopt some form of lights-out operation by year-end.

The two halves of this wave are arriving on different timelines. China is operationalizing the boring version (fixed-cell automation in narrow domains, very mature) at unprecedented scale. The US is trying to ship the harder version (general-purpose humanoids that can be dropped into varied environments). Both halves are moving, both halves are real, and they’re going to meet somewhere in the next five years.

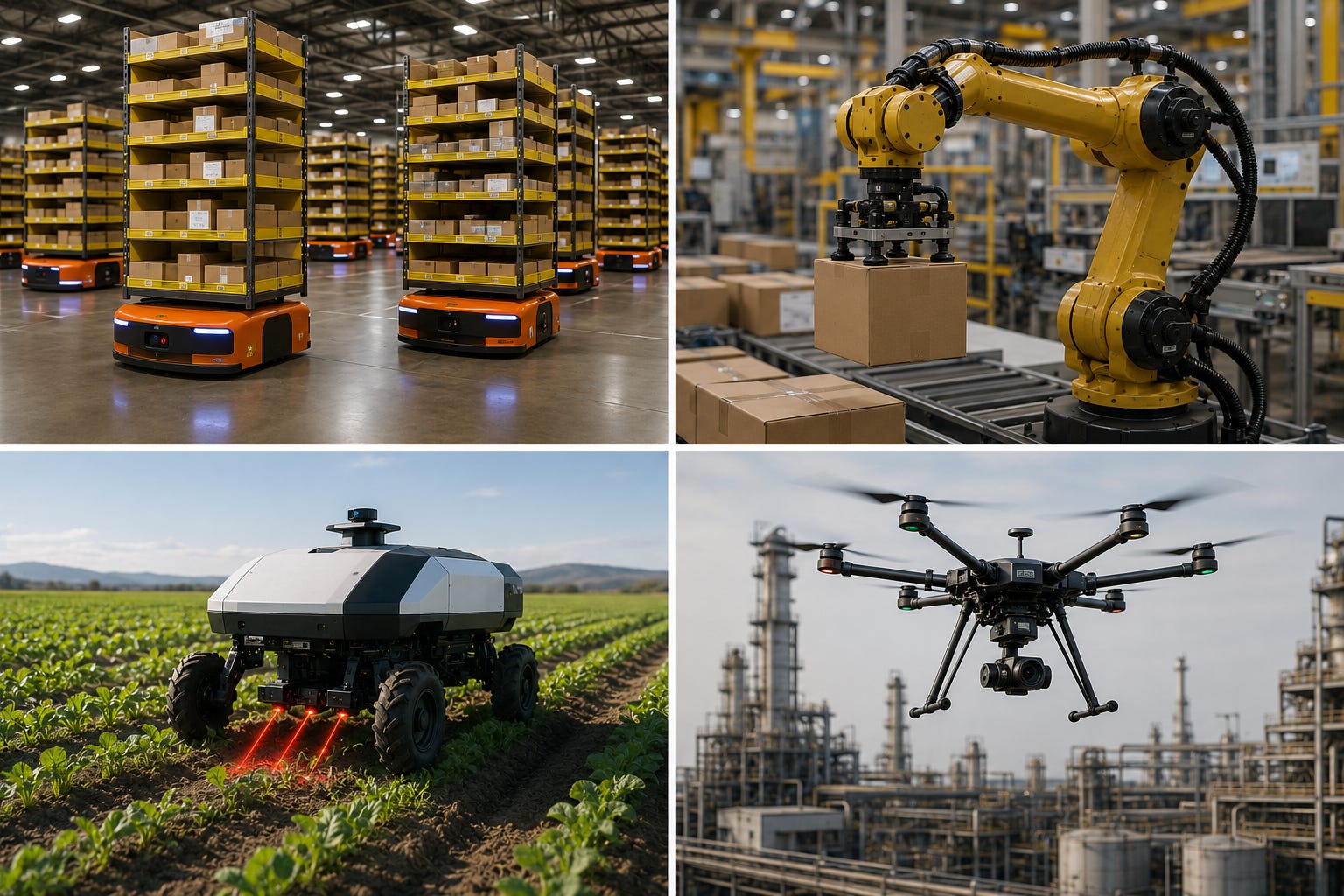

And notice the shape of the thing doing the work, because this is where our imagination tends to fail. Say robots and everyone pictures a humanoid, two arms, two legs, a face. Almost none of what’s actually winning looks like that. Amazon crossed a million robots in its warehouses last year, and not one of them is an android. They’re wheeled carts (i.e. Roombas-looking!!) that slide under a shelf, arms bolted to a table that repeat a single pick a few million times, a machine whose entire job is to move a box from here to there. Out in the fields, Carbon Robotics’ LaserWeeder rolls down crop rows and kills five thousand weeds a minute by zapping them with lasers, no chemicals, no human shape anywhere on it. The most successful robots tend to be the ones we stop calling robots once they work.

A dishwasher is a robot. An elevator is a robot that quietly retired the job of elevator operator and then disappeared into the wall.

The first real wave of physical AI is probably going to look like that, boring, single-purpose, almost invisible, and far more effective for being so narrow. The humanoid is the hardest and most general version, which is exactly why it’s the one we fixate on and probably the one that arrives last.

The case against all of this is stronger than the build-out makes it look

I keep having to argue with a skeptic in my own head, and the skeptic has a name. Hans Moravec noticed something in the 1980s that has aged frighteningly well. The things that feel hard to us, chess, calculus, writing a clean paragraph, turn out to be easy for machines. The things that feel effortless, picking up an unfamiliar object, walking across a cluttered room, folding a towel, turn out to be the hardest things in the world to automate. A billion years of evolution tuned our hands and our balance and almost none of it tuned our algebra.

That asymmetry is exactly why the digital wave moved so fast, and exactly why the physical one might not.

Look closely at the dark factories and the skeptic gets louder. Xiaomi’s plant and the Chinese textile lines aren’t general intelligence wearing a body. They’re fixed-cell automation, one narrow task repeated in a controlled space, and we’ve had a version of that since the Japanese were running lights-out machining floors in the 1980s. The genuinely new thing, a robot you can drop into a room it has never seen and trust to figure out what to do, is the thing that mostly doesn’t work yet. The thousand Optimus units are doing simple, repetitive handling, the easy end of Moravec’s curve.

The best evidence for how hard the rest of the curve is comes from the company now promising a million humanoids a year. When Tesla was building the Model 3, Musk tried to automate almost the entire line, the factory he’d called the alien dreadnought, so robotic it would supposedly look alien to a human eye. It nearly sank the company. The things that kept jamming the line were mundane: soft, floppy parts, fiddly placements, the kind of move a bored teenager makes without looking and a robot fails at all day. He ripped out what he described as a crazy, complex network of conveyor belts and put people back. In 2018 he said it out loud on Twitter, which for him is its own kind of confession: “Yes, excessive automation at Tesla was a mistake. To be precise, my mistake. Humans are underrated.” The lesson is the uncomfortable one for my own thesis. Sometimes a human hand isn’t the inefficient placeholder waiting to be automated. It’s the cheapest, most general-purpose robot ever built, and evolution did the R&D for free over a few million years. Beating it on price and flexibility is a much taller order than a spec sheet of humanoid valuations makes it look.

So the honest version of my thesis is narrower than my excitement wants it to be. The substrate is being poured fast. The general-purpose machine that’s supposed to sit on top of it is still mostly a promise. What I can’t decide is whether the gap between those two things is five years or twenty, and the difference between those two numbers is the whole argument.

What changes when labor stops being the dominant variable

Grant me the optimistic read for a moment, just to see where it goes.

For about seventy years, the math for where you put a factory has been roughly the same. You go where labor is cheapest, holding logistics and political risk constant. That math drove production into Japan, then Korea, then China, then increasingly into Vietnam and Bangladesh. Whole national strategies were built around being the next low-wage hub. Whole post-industrial discourses in the West were built around mourning the wages that left.

If labor stops being the dominant variable, that math inverts. You stop optimizing for the cost of the workforce because the workforce isn’t really the cost anymore. You start optimizing for the cost of electricity, which is why the China electrons post I wrote last year sits underneath this argument like a load-bearing wall.

You start optimizing for proximity to consumers, for political stability, for regulatory speed, for water and cooling, for the things you can’t move.

The Western reshoring conversation makes a lot more sense once you read it through this lens. The intent is to build factories wherever the electrons and the permits work, and to accept that the jobs that come with them will be a small fraction of what left. That’s a politically uncomfortable framing, which is why the public version stays vague. It explains why every serious industrial policy person has gone quiet on the headcount question and loud on the capex question.

Europe is the part I keep turning over in my head. We have terrible electrons, which is bad. We have decent capital, good permitting in some places, dense logistics, and stable institutions, which is potentially fine. The honest answer is I don’t know which of those wins out. The question itself has changed, though, and almost nobody in European policy seems to have noticed.

Why space stops sounding stupid

This is the part where I have to take a small breath, because the argument I’m about to make sounded crazy to me 2 years ago.

Start with what’s already commercial. Varda Space Industries spent the last three years proving you can run a small pharmaceutical manufacturing loop in orbit, send the product back to Earth in a re-entry capsule, and have a paying customer waiting on the other end. They’re working with United Therapeutics on novel crystal forms of existing drugs, the kind of polymorphs you can only get reliably in microgravity. They raised a one-hundred-and-eighty-seven-million-dollar Series C in 2025.

Astral Materials is growing silicon crystals in orbit this quarter under a NASA program, targeting semiconductor wafers that can’t be produced to the same purity on the ground. A few other companies are working on optical fibers (ZBLAN, the kind you’d want in a high-end data center) that come out cleaner when they’re drawn in zero-g.

The boring version of the space manufacturing argument is that there are specific materials whose value per kilogram is high enough, and whose quality is sensitive enough to gravity and air, that orbit is just a better factory floor for them. That’s already true. The capex math works for pharmaceuticals today. Starship pushes it toward sub-five-hundred-dollar-per-kilogram launch, with credible scenarios for sub-one-hundred-dollar-per-kilogram in the back half of the decade. At those numbers, the list of materials worth making upstairs gets a lot longer.

Now the bolder version. The reason orbital factories always sounded ridiculous came down to one assumption: you needed humans up there to run them, and humans in space are absurdly expensive. Take the humans out of the equation, which is exactly what’s happening on the ground right now, and the question changes. If a factory can run itself, you stop asking “where can we afford to put the workers?” and start asking “where would I put this thing if I optimized for vacuum, microgravity, energy access, thermal environment, and the absence of regulation that hasn’t caught up yet?”

For a non-trivial set of products, the answer is going to be: above the atmosphere. Asparouhov, Varda’s founder, talks openly about an industrial park in orbit. The first time I heard him say it, I rolled my eyes a little. The second time, I went back and did the math. The math is closer than I was comfortable with.

What we’ll have been wrong about

Five years from now, I think the AI conversation of 2025 and 2026 is going to read the way the dial-up internet conversation of 1998 reads now: genuine, important, formative, and not the main story.

The main story will turn out to be the moment the language models stopped being the bottleneck and the bottleneck moved to the actuators, the cameras, the joints, the warehouses, the factories, the rockets. The moment, in other words, that the physical world started compounding the way the digital one did thirty years ago.

I think we’re in the flat part of the curve right now. The part where the substrate is being laid down quietly. The part where Xiaomi runs one plant, Varda makes one drug, Tesla deploys one thousand humanoids, and none of it looks like a revolution because revolutions look like infrastructure work right up until they don’t.

The freezer behind the counter

I want to come back to my friend’s gelateria, because the original framing has aged in a way I didn’t expect.

The people in that gelateria are still safe. The Pilates studio is still safe. The doctor sitting across from you, watching your face, is still safe. The argument I made then was right about where the value lives in those settings. What I missed is that almost everything behind them, the freezer, the supply chain feeding the freezer, the factory that built the freezer, the truck that delivered it, the chip in the controller, the rare earth in the chip, the orbit-grown crystal that might one day sit in the chip, all of that is going to be touched by this next wave in a way the previous wave didn’t quite reach.

The boundary moves while the visible thing stays put. What I keep coming back to is how fast the line is moving, and whether the conversation we’re all having right now helps us see the next wave coming, or sets us up to miss it the same way we missed the last one while it was happening.

One last thing, because predictions like this are so easy to wave away. The hardest thing for any of us to do is picture a present that looks genuinely unlike the one we’re standing in. We round the future off to the past. But between what I’m watching now and what I wrote a month ago, I’ve stopped hedging on one point: the robots are closer than almost anyone outside this world believes. I still can’t tell you what that will mean, and anyone who says they can is guessing. The timing is the part I’m sure of. Three years from now, the ground under all of this is going to look very different from today.

Have a great weekend!

Giovanni