To Buy or Not to Buy

To Buy or Not to Buy

#77 - Should You Rent or Invest in Buying a Home?

Hello friends, I hope you’re doing great! This is probably the post that will cause most controversy, given the sensitivity of the topic and its relatability with basically everyone: should I buy or rent my home?

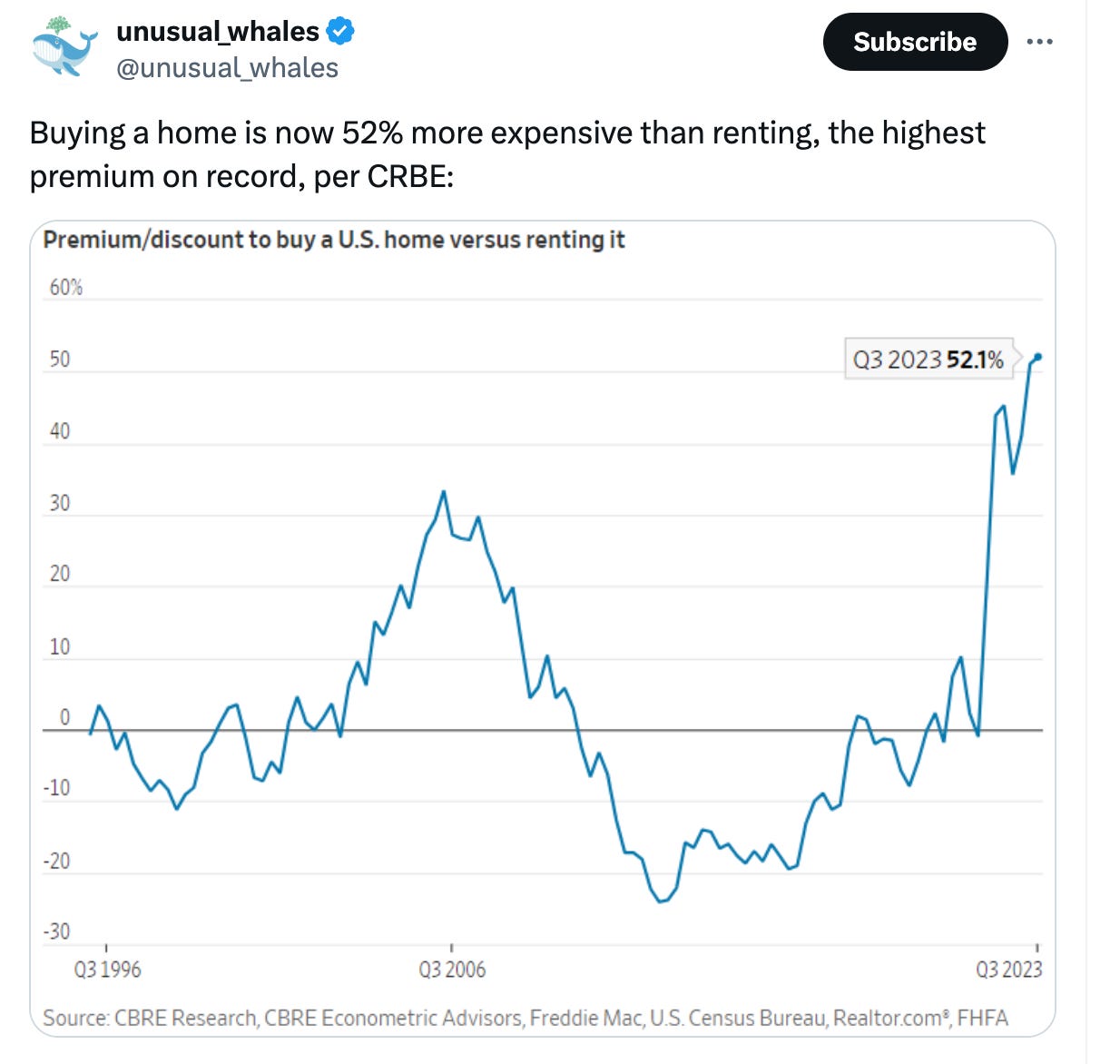

I have always been thinking about this a lot, but the idea to write this post came actually from seeing this tweet:

I have read and investigated a bit on the topic, trying to form a more “data-driven” and objective opinion and more importantly trying to appreciate the many nuances behind the topic.

In recent years the traditional view of homeownership has undergone a significant transformation. Once seen as a universal goal, the decision to buy a home has become more nuanced, influenced by a complex mix of economic factors, personal circumstances, and shifting societal values.

For many, especially Millennials and younger generations, owning a home has started to feel like a distant dream. Factors such as soaring home prices, fluctuating interest rates, and the evolving nature of work and lifestyles have made this key life decision more challenging than ever.

I have particularly liked this podcast, where the authors provide an interesting perspective on the topic, trying to maintain a detached view and using financials to argument their position, but also acknowledging how buying a home is not only a financial decision, but most importantly a personal investment that has implications that exceed only the return on the investment!

The podcast episode’s title (“Why Buying A House Makes Zero Financial Sense”) gives away the position of the authors but then their view is a lot more nuanced and I feel like it provides a lot of interesting insights into the discussion that I tried to recap in this post.

Most of the data in this post are based on the US market situation, because that’s where I found most of information on, but I think that the conclusions apply by and large to global western markets.

Analyzing the Financials: Renting vs. Buying

In the podcast the author makes a very good point, that might sound basic but that I think is too often overlooked in these discussions: when I buy a steak, or go out for sushi, I do not do an ROI calculation and take a decision based on that. I just go out and enjoy the dinner, even if I understand that financially that wasn’t a good decision (i.e. cooking is surely cheaper). That’s what life is made of, and everyone has a different compass about what brings them joy.

So not everything in the discussion of renting vs buying a house should be based on financial considerations.

Having said that, I feel that financial considerations for what for many people is the largest purchase of their life are indeed very relevant. And I think that a lot of the narrative around Real Estate is based on misconceptions and under-appreciated points, that I feel would benefit from some clarity. I will try to lay out the key points I noted when thinking about this, and then try to explain them through a quantitative example.

Initial and Maintenance Costs

When you buy a home, the initial financial burden includes the down payment, often a significant percentage of the home’s price, and closing costs that cover various fees. These amounts vary with different market considerations, but the upfront expenses can be substantial. Then there are yearly maintenance costs, that directionally amount to 2% of the property value.

Mortgages and equity building

Mortgages are a complex financial product, with the majority of initial payments going toward interest rather than the principal. This dynamic means that in the early years of a mortgage, you’re not building as much equity in the home as you might think.

This is the main financial counter-argument for the “if you rent you’re throwing money out of the window, you should be building equity through mortgage instead”.

Using a 30-year mortgage as an example, it’s surprising how much of your initial payments go towards interest, delaying significant equity building: after 10 years you have “only” accumulated 25% of the mortgage total as capital payment, the rest is interests!

Opportunity Costs

Opportunity cost, arguably the most elusive concept in our discussion, is fundamental yet often difficult to fully comprehend. At its core, it refers to the potential gains you forego when you allocate capital to a specific investment. In the context of home ownership, the primary opportunity cost lies in what you might have earned had you invested your downpayment in an alternative asset, such as the equity market. This consideration is crucial; it's not merely about the money spent on buying a home, but also about the potential returns from other investments that you might miss out on by channeling your funds into real estate.

Inflation

This is again a very “basic” concept, yet one that I think is very hard to visualize: when talking about home prices and their growth, we often refer to “nominal” prices (i.e. the price at which the transaction happens), but doing this we ignore the impact of inflation, which can cumulatively be very material over long term horizons.

In other words, if the house’ price has gone up +50% in 20 years, but inflation grew 40% the real “net” growth is only 10%. And this ties back to the opportunity cost discussion, when comparing the house purchase Return On Investment (ROI) and the opportunity cost you should make sure to compare apples-to-apples.

It’s very easy to “fool yourself” in saying things like “house price grew 20% in 5 years, it’s booming!”, because if in the same period inflation grew 18% and, as often the case, the return on investment in stocks or bonds is above inflation you actually lost money (in real terms, not nominal) by buying.

The magic number

Investigating on the topic of renting vs buying there’s a common number that you hear from all the experts: 25. And this is the efficient frontier above which is not worth buying, and renting is actually a better financial decision.

This number is simply the ratio between the purchase price of a house divided by its yearly rent.

I am naturally skeptical about these “magic formulas”, especially for things that have such a high level of ambiguity like buying a house and that depend on so many factors. I therefore did what I was trained to do: I built an excel model where I tried to calculate what was the “efficient frontier” (i.e. the price point where it starts being more efficient to rent) and… I validated the number, they’re right! 25 is the right number!!

Let me explain why and what I did.

I took some assumptions, using round numbers for simplicity, and built 2 “personas”: Mr Buyer and Mr Renter.

Mr Renter spends $36k/year in rent, and invests the “house downpayment savings” in the equity market (I used the average returns of S&P500 for the last 30 years, which are 9.90% yearly);

Mr Buyer instead, decided to buy the same house Mr Renter lives in (which is on the market for $1MM) and took a mortgage that costs roughly the same yearly amount as Mr Renter (with a fixed interest rate of 2.7%, current estimation on Zillow), because they have the same budget. He obviously puts down a downpayment ($450k) because the yearly rent he can afford won’t cover a higher share of the price.

I then took a few assumptions:

Mr Renter sees his yearly rent increase every year by the inflation rate (3%);

Mr Buyer sees an appreciation in value of his house of 5% yearly (last 30 years data in the US was 4.94%);

Mr Buyer spends 5% of the purchase price as transaction cost, at purchase moment;

Mr Buyer spends 2% of house value every year in maintenance (historical average from US housing data).

And then I fast-forwarded 30 years into the future, and discounted the cash flows to today.

And the result was exactly what the podcast hosts were commenting: Mr Renter was richer, a lot richer, than Mr Buyer. Renting has been generating to Mr Renter $642k more than Mr Buyer. When you read the assumptions this sounds very intuitive: investing $450k (the downpayment) on the stock market, to generate 9.9% yearly returns for 30 years, vs putting it in a downpayment of an asset that yelds 5% yearly…. clearly makes a difference over the years.

So, I wondered, is it always less convenient to buy than renting? To answer that question I modelled an alternative story: the cousins of Mr Buyer and Mr Renter, that decided to move from the center of a major city to suburban smaller town, where rent and house pricing are different. And the results were starkly different: mr suburban-Buyer had generated over a $1MM more than Mr suburban-Renter!! How is that possible? Well there are some very simple explanations:

In the last 20 years house prices in suburb locations grew a lot more than central major cities (9% vs 5%). So buying creates a lot more asset value repricing;

Since the amounts are smaller, because house prices are in absolute value lower in suburb location vs major cities, the upside of investing in the equity market the downpayment ($80k, over a $400k house purchase) basically covers for the rent;

Most importantly: the famous price/rent ratio is a lot lower in secondary locations, making the investment a lot more appetible.

The conclusion is actually quite intuitive, and what you can see represented in this table below: when you look at house rent and purchase prices in american cities, you basically can split them in 2 buckets, above or below 25 Price-to-Rent ratio. In the first bucket, when home price is over 25x the yearly rent, buying is not a financially savvy decision, on the lower bucket instead the contrary is true.

I am not sure about how robust this 25 ratio is, nor what has been the historical evolution, but it sounds like a very simple, yet reasonable high-level KPI to assess the financial viability of buying vs renting before even considering all the other factors like mortgage amount, rate of interest, cost of transaction, etc.

Debunking Myths and Misconceptions

With all the above said, I thought there are some myths and misconceptions that the podcast helped me debunk.

Myth 1: Renting Is Just Throwing Money Away

This common misconception suggests that renting offers no long-term financial benefits. However, renting can often be the more prudent financial decision, particularly in markets where buying is significantly more expensive. As proven by my example renting could be in many instances the better decision, from a financial stand-point.

Myth 2: Buying Is Always a Great Investment

Homeownership is often viewed as a surefire path to building wealth, but this isn't always the case. While owning a home can lead to equity building and potential property appreciation, these outcomes are not guaranteed. The housing market can be volatile, and factors like location, market timing, price and interest rates significantly impact the actual return on a home investment.

Myth 3: The Bigger, the Better

There’s a notion that when it comes to buying a house, bigger and more expensive is always better. This belief can lead to overextending financially to acquire a property that exceeds one's needs or budget. In the podcast the hosts actually make a very interesting comment: often when renting you can be more frugal. When buying a house, given the large amounts of money involved it’s easy to think “well, let’s buy a bit bigger than we can afford” as the delta in price is diluted in the 20/30 years repayment plan of the mortgage. When renting instead, getting a higher rent usually means giving up something in the short term (e.g. “if I pay xx more in monthly rent, I won’t be able to go to that nice vacation I wanted this summer”), thus often resulting in being more frugal.

Myth 4: Renting Offers No Stability

Renting is often unfairly associated with a lack of stability or permanence. However, many renters enjoy stable living environments, with long-term leases and the ability to make their rented space feel like home. Additionally, the flexibility of renting can provide a form of stability in itself, particularly for those who value the ability to adapt and move as their life circumstances change (my family and I changed 3 cities, and over 10 houses in the last 15 years, yet we feel very stable and united as a family!).

Money is not the most important thing in life!

As I close this post there’s a key point I want to make: I focused most of this post on the financial implications of buying vs renting, but I actually think that financials are only one of the many variables embedded in this decision. As the authors of the various sources I read stress, buying a home is not just a financial transaction; it’s a deeply personal choice that encompasses our aspirations, lifestyle, family goals, and sense of security.

It’s about creating a space that resonates with our deepest desires for comfort, stability, and belonging. While financial indicators are important and provide a framework for understanding the implications of our choices, they cannot fully encapsulate the emotional and psychological aspects of creating a home.

As such, when facing this choice, it’s essential to weigh both the tangible and intangible factors, understanding that some of the most significant benefits of homeownership are, indeed, beyond measure.

The best decision is the one that aligns with your unique circumstances, values, and vision for the future.

I wish you a fantastic weekend!

Giovanni